Can you imagine living without paying rent or a mortgage?

Can you imagine living without paying rent or a mortgage?

For many, the idea of living without paying rent sounds like an impossible dream. In an era where housing costs consume a huge portion of our income, finding a way to eliminate this expense could lead to true financial freedom.

However, while the concept is appealing, the legal realities behind it are often complex and involve significant risks that every occupant should understand.

1. The Reality of Adverse Possession

In the legal world, the most common way people attempt living without paying rent in a property they don’t own is through a concept called “Adverse Possession.” This law allows a person to claim ownership of a property if they have occupied it openly and continuously for a specific number of years. However, this is not a “get out of jail free” card. Every state has strict requirements, and failing to meet even one can lead to immediate eviction.

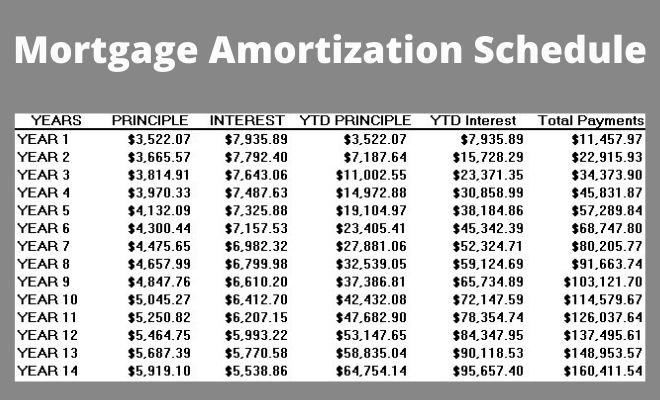

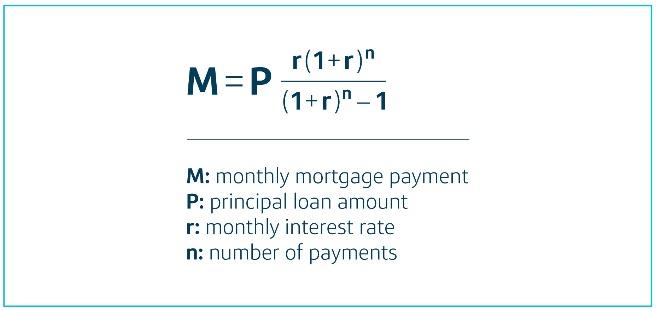

If your mortgage payment is $1,420, aim to pay $1,500 whenever possible.

The key is making sure the extra amount is applied to PRINCIPAL ONLY.

Small monthly increases reduce the loan balance faster and save thousands in interest.

3. use your tax refund strategically

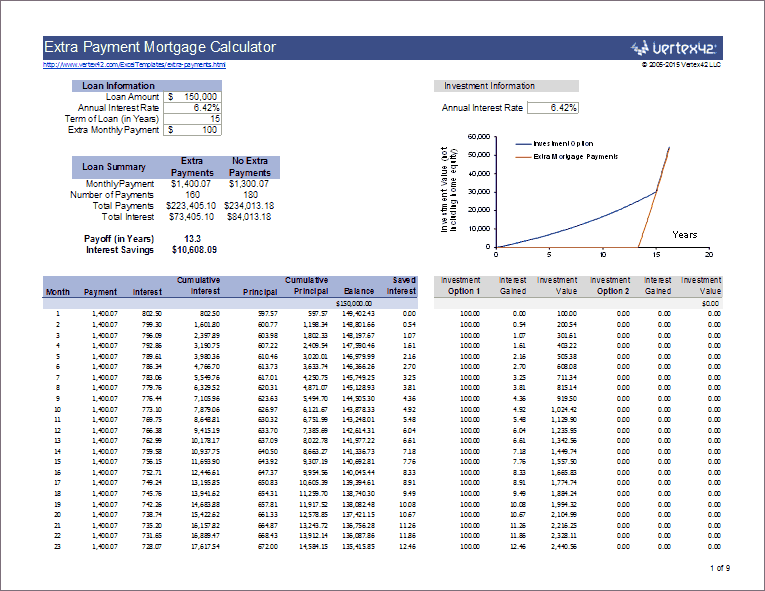

Tax refunds and bonuses are powerful financial tools.

Applying a lump-sum payment to the principal once a year lowers the balance used to calculate future interest, creating long-term savings.

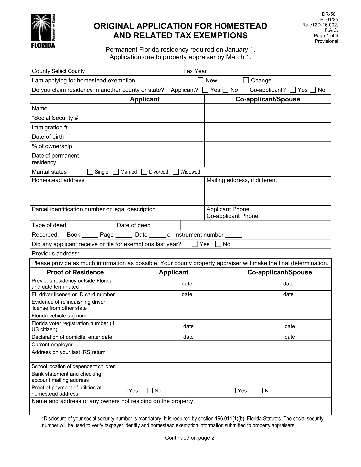

4. florida homestead exemption

If your home is your primary residence, Florida’s Homestead Exemption can reduce property taxes.

Lower escrow payments allow more of your monthly payment to go toward the principal.

Many homeowners qualify without realizing it.

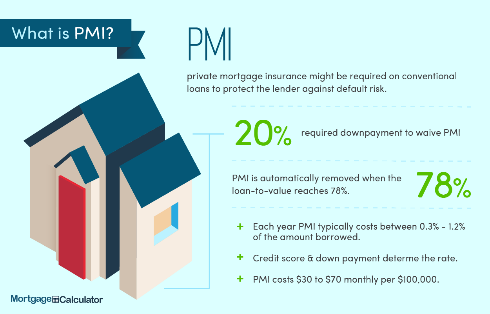

5. eliminate private mortgage insurance (pmi)

PMI protects the lender—not you.

Once you reach 20% equity, you have the right to request PMI removal.

With rising property values, many homeowners already qualify.

6. refinance only when the math makes sense

Lower interest rates can help—but only if refinancing is done correctly.

Avoid restarting a 30-year term. Match the new loan term to your remaining years and always review closing costs.

7. turn a side hustle into a mortgage accelerator

Small businesses such as food sales, crafts, cleaning services, or consulting can generate extra income.

Directing those profits toward your mortgage can eliminate debt years earlier.

8. review your escrow account annually

Banks sometimes miscalculate escrow payments.

Reviewing your annual statement ensures you are not overpaying unnecessarily.

Please note that this applies to the family home, with the following exceptions:

If you are a widow or surviving spouse, you may be eligible for an additional exemption, Surviving Spouse or Minor Children

After the death of the homeowner:

The surviving spouse retains the homestead protection.

Minor children may retain rights to the family home.

The property may be protected from forced sale by creditors.

This applies even if the survivor was not originally listed on the property title, and if you are a disabled veteran or a homeowner with special status. Disabled Veterans and Homeowners with Special Status.

Some homeowners qualify for expanded exemptions, even beyond the standard homestead exemption:

Veterans with a total and permanent disability

First responders (under certain conditions)

Surviving spouses of veterans or first responders

This may result in total property tax exemptions.

final advice – balance freedom with security

Paying off your home early is powerful, but never eliminate your emergency fund. True financial freedom includes low debt and strong savings.

Clara Mercado Legal Document Preparer & Notary Public Orlando, Florida

Contact us today for a consultation. We help you navigate the complexities of property law so you can focus on building your future!

NOTE: I am not an attorney and do not provide legal advice. I share verified, current information about legal documentation and financial literacy in the United States.